Allocation of Audit Resources

This year's allocation of resources is based on our current staffing complement of 13 FTE auditors, and an assumption that we will hire at least one additional auditor by January 2024, for a total of 13.5 FTE auditors for FY24 (see FY 2024 Staffing below for more details).

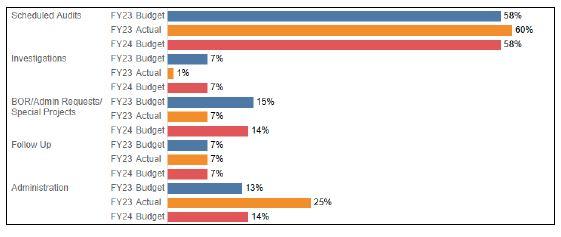

At 13.5 FTEs, approximately 58% of the Office of Internal Audit’s resources will be committed to the completion of planned audit projects. This year 6% of those resources will be needed to complete carry-over work on the five audits started in FY 2023 that will be reported in FY 2024.

The remainder of our FY 2024 audit resources is reserved as follows:

- 7% has been reserved for investigations. The number of hours remains consistent with previous years.

- 14% has been reserved to accommodate special requests and projects including senior leader transition audits, SNAP reviews and requests from the President, the Board, or members of the senior leadership team. The number of hours remains consistent with the previous year.

- 7% has been reserved for follow-up procedures on outstanding report issues performed on behalf of the Audit and Compliance Committee. The number of hours remains consistent with previous years.

- 14% has been set aside for internal administrative functions, including staff oversight, hiring and onboarding; annual audit planning; data analytics; and other continuous improvement efforts. This is an expected reduction in time. Last year we experienced significant staffing turnover including in the leadership team that was temporarily filled by an auditor assuming an interim audit director role. We expect time will continue to be needed of hiring and onboarding, but we expect less turnover and maintaining higher overall staffing levels will result in a higher percent of time spent on other audit work.

Reliance on Other Providers

To avoid duplication of work and reduce burden on University staff, we continue to place reliance on audit-related work performed by other service providers. We rely on the external audit work performed by Deloitte, LLP in the areas of investments, annual external financial reporting, and RUMINCO (the University’s captive insurance company). Deloitte, LLP also provides significant coverage of student financial aid as part of its Uniform Guidance Audit, which we take into consideration in our risk assessment.

We also rely on the audit work performed by external construction audit firms engaged by the University’s Capital Planning and Project Management (CPPM) unit for construction projects that are delivered using the Design/Build or the Construction Manager at Risk delivery methods. We are in agreement with the scope of this audit work and receive and review copies of their reports.

Recap of FY 2023 Internal Audit Results

Our audit planning begins with a review of past audit coverage and results. Appendix A recaps the audits completed for the last three fiscal years and the resulting overall control assessments. Appendix B details progress made against the FY 2023 audit plan and other audit work performed. To date, we have completed 24 audits in FY 2023. The risk management and control environments of 16% of the activities audited were rated as "Needs Improvement." The remaining 84% of audits were rated "Good" or "Adequate." These results continue to demonstrate an overall culture of compliance and risk management throughout the University.

In addition to the 24 audits completed:

- Audits in Progress: 4 - audits are currently in progress and plan to be completed in FY 2023.

- Completed Next FY: 5 - audits are in progress and will be completed in FY 2024.

- SNAP Reviews: 3 - SNAP reviews were issued.

- Deferred Audits: 4 - Tier 2 audits from the FY 2023 audit plan were deferred to FY 2024 and 2 additional audits were added as communicated to the Committee in February. The FY 2023 audit plan was built on the expectation of hiring all but one open position by the end of December 2022. Although we successfully hired most open positions, one IT audit position was not filled until March 2023, and an additional financial auditor left the department this spring. This limited our ability to replace some deferred audit work especially related to IT.

- Audits Deferred to FY 2024: Parking & Transportation Services, Central Cloud Platform; Minnesota Supercomputing Institute,; and Gramm-Leach-Bliley Act (GLBA)

- Replacement Audit Work: Institute on the Environment (IonE), and Aerospace Engineering & Mechanics

- Employee Surveys: 36 - employee surveys were sent out to 1085 participants as part of regular unit audit processes, with a 70% response rate.

- Investigations: 7 - investigations into financial or operational misconduct were conducted in accordance with the University Policy on Reporting and Addressing Concerns of Misconduct. OIA partnered as appropriate with the University of Minnesota Police Department (UMPD), Office of the General Counsel, Office of Institutional Compliance, Research Intelligence & Compliance Team, and other units to complete these reviews.

Independence

Coordination with Other Internal University Resources

Compliance Partners

The Office of Internal Audit coordinates its work with other internal units to maximize the quality of audit coverage provided, as well as to promote prompt attention when University-wide trends are identified. We have established strong working relationships with the University’s compliance partners, including: the Risk Intelligence and Compliance Team; the Human Research Protection Program; Health, Safety & Risk Management; University Information Security, the Health Information Privacy & Compliance Office; and the Office of the General Counsel. We work closely with each of these units during audits involving complex regulatory issues.

The Office of Internal Audit interfaces regularly with the Institutional Compliance Officer and we serve on the Executive Compliance Oversight Committee. Input from the Compliance Officer is also solicited during our annual audit planning. In addition, throughout the year we report to and collaborate with the Compliance Officer on issues identified during our audits. We also share the results of employee surveys conducted during audits with the Compliance Officer. Along with the Office of Institutional Compliance, we serve on the triage team for managing UReport, the University’s anonymous hotline. We are also working with the Office of Institutional Compliance to ensure that duplication does not occur between their risk assessments and audits. Both offices are committed to sharing information and leveraging each other’s work as appropriate to optimize resource usage and reduce impact on units involved.

Policy & Process Owners

Audit results are shared with policy owners and central support units such as the Office of Information Technology, Sponsored Projects Administration, Controller’s Office, and the Office of Human Resources when policy non-compliance or the need for process enhancements are identified. In addition, best practices identified in local unit audits are shared with these central unit process owners for consideration of broader adoption. We also have regular meetings with leadership and other representatives from these offices to discuss audit results and trends, changes in regulations, policy interpretations, etc.

Enterprise Risk Management and PEAK Initiatives

Enterprise Risk Management (ERM) and Positioned for Excellence, Alignment and Knowledge (PEAK) are two major initiatives with current and future impacts to the audit function in the years ahead. The Chief Auditor is a member of the ERM Task Force and the PEAK Steering Committee to ensure we stay abreast of these initiatives. In FY 2024 we expect ERM will work with University leadership and the Board of Regents to establish new institutional risk profile. We will ensure our audit work remains in alignment with the highest risks identified through this process. In addition, we expect ERM to play a larger and more consistent role in the Audit and Compliance Committee, which is responsible for overseeing it. As PEAK implementation continues and streamlines administrative activities, it will likely continue to affect various process audits, risk levels and audit scoping in some unit audits. It may also impact the timelines of issue remediation as units elect to resolve issues identified in audits as part of broader PEAK efforts. In FY 2023 OIA implemented a regular report as part of our Internal Audit Activity update detailing issues management identified would be addressed as part of changes associated with PEAK. We will continue to update and maintain this document in FY 2024. As PEAK is implemented, we will also consider adjusting our audit work to ensure ongoing optimization of audit coverage, we will keep the Committee informed of any significant trends as they emerge.

Staff Development Qualifications and Professional Development

The Office of Internal Audit is committed to providing educational opportunities to our staff in order to continually enhance our audit knowledge and abilities. Ever-changing government regulations, new technologies, and new developments in auditing principles and methods dramatically affect not only what we audit, but how we audit. We strive to stay abreast of new developments and improve our audit proficiency to enhance the overall quality of our audits. To accomplish this, we pursue a variety of methods to continue our staff's professional education. Our memberships with the Institute of Internal Auditors (IIA), the Association of College and University Auditors (ACUA), the Association of Certified Fraud Examiners (ACFE), the American Institute of Certified Public Accountants (AICPA), and ISACA provide staff members the opportunity to attend seminars and conferences that specifically address current issues and techniques in internal auditing. The interaction of our staff members with their peers through these professional organizations helps to keep us up‑to‑date on the latest auditing trends and issues affecting higher education.

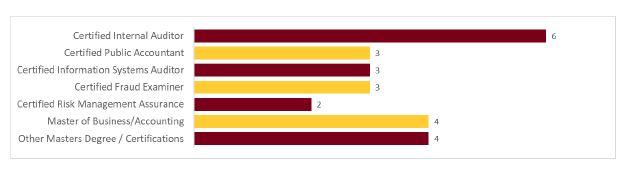

All but three of our internal audit staff are professionally credentialed or hold advanced degrees,. the remaining three have been with OIA less than a year and one is in the process of obtaining credentials. The number and combinations of certifications held by staff demonstrates a high-level of competency in the skills needed to provide quality audit work in the University’s complex environment.

In the first 10 months of FY 2023, the Office of Internal Audit provided approximately 1,000 hours of formal and informal training. These hours do not include the time associated with competing coursework partially funded by the University's Regents Scholarship Program. For FY 2024, 1,150 hours have been budgeted for staff training. This ongoing training also provides the continuing professional development required to maintain the staff's professional credentials.

Professional Standards

Internal Quality Assurance Program

External Quality Assurance Review

Office of Internal Audit FY 2024 Staffing

When fully staffed we have 16 auditors (9 financial/operational auditors, 2 IT auditors, 1 senior data analyst, 1 associate audit director, and 3 audit directors) in addition to the Chief Auditor. OIA has experienced an unusually high level of turnover in the last 18 months consistent with broader employment rends. We have worked to onboard five new auditors since April of 2022 including a new IT audit director. We are actively recurring for two open financial/operational auditors with the assistance of the Office of Human Resources' Talent Acquisition team. Our Audit Plan is built with the expectation that we will have hired at least one of these positions by January 2024.